Selling benefits should not be a one-size-fits-all solution – not if you’re looking for profitable clients, that is. Prospects of different sizes have differing needs, and that warrants a unique approach when selling to a business with 50 employees compared to a business with 500.

Small businesses, in particular, present significant opportunities for benefits advisors. Ontario alone is home to just short of 450,000 businesses, and an incredible 97% of those businesses have fewer than 100 full-time employees.

Even within that <100 employee grouping we can get more specific and more intentional with our sales approach. We’ve already touched on selling to businesses with 1 to 5 employees and selling to businesses with 5 to 20 employees, so in this article, we’ll discuss how to best sell benefits to those profitable clients with 20 to 100 employees.

How to Provide Value-Added Service at a Profit for Clients with 20 to 100 Employees

We know that it’s important to adapt your sales approach based on the nature of the prospect’s business, but how exactly do you do that? It’s all about figuring out what’s important to that business and then building a custom plan that prioritizes those values. Here’s how:

1. Client Needs Analysis

First of all, you need to understand your prospect’s goals and where the business is headed. The best way to figure this out is to simply ask! By asking future-based questions, your prospect will effectively give you a road map for where their business is hoping to go, which you can then use to craft an individualized benefits plan to suit their specific needs and objectives.

An effective benefits plan will look different depending on the client’s goals: if the client is planning to merge, to sell, to retire, to grow, to enter new markets, and so on. A great way to determine exactly what’s important to the prospect is by using Dan Sullivan’s future-based question:

“If we were meeting here three years from now and you were looking back over those three years, what has to have happened to say those were the best three years of your life?”

Use their answer to dictate how you approach the benefits plan and the sale as a whole. If they don’t provide a valuable answer or if they’re unwilling to engage, simply move along to the next prospect! Remember, small businesses in Ontario are abundant and as a benefits advisor, your time and energy is best spent with profitable clients. Prospects who are unwilling to engage with you and let you into their goals and values are not profitable clients, so your best option is to simply move along and focus on those prospects who allow you to provide value to their employees and generate a profit.

2. Understanding Risks and How to Manage Them

What is a benefits plan if not a promise that an employer makes to their employees? Framing benefits in this way is highly effective in guiding a prospect in the right direction and shifting their perspective on what a benefits plan could be. It helps them realize that they have the power to craft a distinct plan that works for their employees and themselves, and it leaves them feeling confident that you’re the advisor to help them do so.

It’s your role as an advisor to translate industry terms and jargon into terms the prospect will understand and that will resonate with them. In general, there are two overarching groups of promises that an employer can make to their employees with regards to employee benefits:

Low-Frequency, High-Cost

Low-frequency, high-cost benefits are those benefits that don’t occur on a regular basis but when they do, they’re expensive. This includes things like group life insurance, group AD&D, long-term disability, critical illness insurance, out of country travel insurance, and stop loss insurance.

These are the promises that require insurance to fulfill.

High-Frequency, Low-Cost

Conversely, these high-frequency, low-cost benefits are those that happen relatively often, but which are less costly when they do. They include extended healthcare, prescription drugs, vision, dental, and short-term disability are all examples of high-frequency, low-cost promises.

These sorts of promises don’t necessarily require insurance however they do require budgeting.

The right solution will depend in each case on the prospect’s needs and desired direction, and it’s your job as their insurance advisor to guide them toward that solution.

The great thing is that clients aren’t obligated to choose between one or the other; you can – and should – create custom, individualized plans that are designed with the client’s unique needs in mind. This sort of approach gives the client a benefits plan that fits like a glove, while also making you an extremely valuable and hard to replace advisor in their eyes.

The most effective way to build a custom plan is to divide the employees into groups. This could be based on the employees’ roles, their time with the company, or any other number of factors. Let’s look to some case studies as examples.

Case Study #1

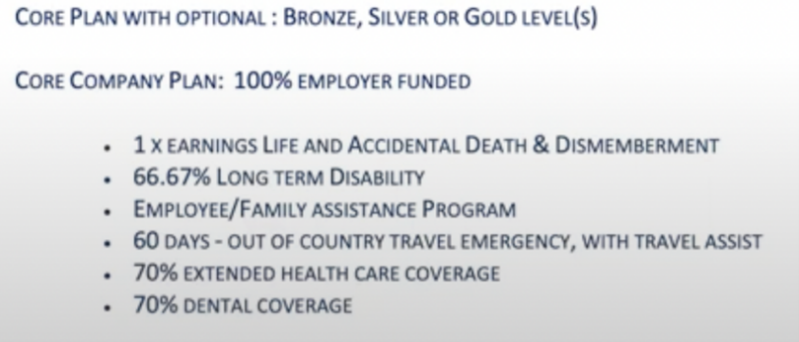

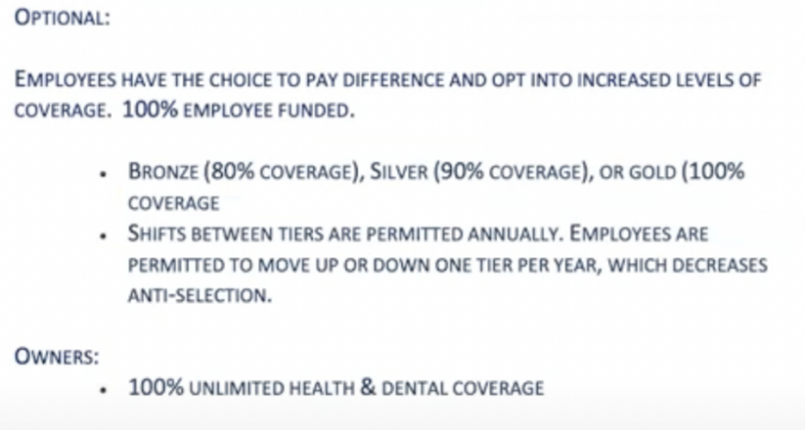

A family-owned business with 62 employees spread across a range of roles with different specialized skillsets and different salaries was looking to build a custom benefits plan that worked for them.

The owner was looking to provide benefits to all of their employees, while also offering a tiered system of optional add-ons that employees could choose to pay in to if they wanted an increased level of coverage.

We built a system with a core company plan that was available to all employees, ensuring that the employer had them covered in the majority of situations. Then, we developed a gold, silver, and bronze system which the employees could choose to participate in based on their own personal situations.

This creative plan design was effective in keeping the client’s budget while ensuring that all of their employees have access to core benefits. The employees had the advantage of a flexible benefits plan that they could mold to meet their personal objectives.

Case Study #2

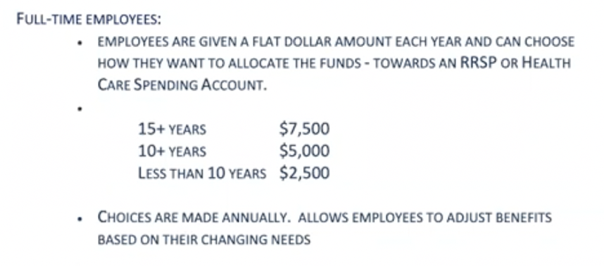

A company with 72 full-time employees and two owners was looking to build a benefits plan that reflected their company philosophies of empowerment and equality. The company had a flat structure where every employee was equally valued, and they wanted a custom benefits plan that reflected that philosophy.

A company with 72 full-time employees and two owners was looking to build a benefits plan that reflected their company philosophies of empowerment and equality. The company had a flat structure where every employee was equally valued, and they wanted a custom benefits plan that reflected that philosophy.

This was achieved by providing a general plan to all employees as well as a flat dollar amount for full-time employees based on their time with the company. This custom solution also allowed for employees to choose how to allocate that flat dollar amount, giving them the choice annually to put the funds toward an RRSP or a healthcare spending account. Employees could choose to utilize the healthcare spending account if they knew their child had upcoming orthodontia needs, for example, or they could place those funds in an RRSP if they didn’t anticipate much use for the healthcare spending account in a particular year.

This was achieved by providing a general plan to all employees as well as a flat dollar amount for full-time employees based on their time with the company. This custom solution also allowed for employees to choose how to allocate that flat dollar amount, giving them the choice annually to put the funds toward an RRSP or a healthcare spending account. Employees could choose to utilize the healthcare spending account if they knew their child had upcoming orthodontia needs, for example, or they could place those funds in an RRSP if they didn’t anticipate much use for the healthcare spending account in a particular year.

This solution allowed the employer to budget effectively and avoid surprises, while the employees were treated fairly across the company and had the power to allocate funds in the way that was most useful for their particular needs.

The key to creating these effective custom solutions lies in asking those crucial future-based questions and determining what’s important to each individual business owner. This will help you to determine what promises they’d like to make to their employees, and you can use that information alongside your benefits expertise to craft a unique benefits plan that works for everyone involved.

3. Reporting and Accounting Considerations

The next thing to keep in mind when selling to businesses with 20 to 100 employees is how to go about reporting. We highly recommend sending each client a detailed report each month which includes how much they’ve paid that month, how much has been paid to insurance companies, the claims that have been made across various categories, the relevant expenses and commissions, and their overall surplus or deficit for the month.

This acts as a sort of itemized receipt for their benefits plan that keeps the client in the loop and eliminates any surprises down the road. Should anything unusual appear on a monthly report, you can have a chat with them to discuss their questions right away and show them the source of the discrepancy.

Clients typically appreciate these monthly reports and the insights that they provide. We also recommend conducting a review of the benefits plan with the client on an annual basis, and these monthly reports ensure that nothing comes as a surprise and enables them to come into that review informed and prepared.

4. Taxation Considerations

Of course, taxes are something to be considered when crafting that perfect plan for a business with 20 to 100 employees.

This primarily comes into play when discussing the benefits provided to the business owners themselves. 100% unlimited plans are extremely effective for business owners, as premiums are a fully tax-deductible business expense. This setup means that the business owners can receive any healthcare that they would have purchased anyways, through a tax-effective approach.

The one exception to this is the case where the spouse of the business owner has their own benefits plan. In this case, a healthcare spending account may be a wiser approach, since healthcare spending accounts act as the second payer and can cover any expenses that are not covered by the spouse’s benefits plan. Otherwise, utilizing a 100% unlimited plan for business owners is highly recommended.

Provide Value for Profitable Clients with 20 to 100 Employees Through a Custom Benefits Plan

Your role as a benefits advisor is all about creating value for your clients. The best way to do this is by crafting custom solutions that are built to meet their particular needs and fit their unique situations! You can do this by asking future-based questions and using the responses as a roadmap to guide you as you craft that custom solution.

Approaching benefits advisory in this way also provides you with profitable clients that are stable, since you’ve provided them with an effective solution that they can’t get elsewhere or replace with an off-the-shelf benefits plan.

The Benefits Trust has almost 30 years of experience providing Third Party Administration services, and we’re here to help! Contact us today for more insights on how to sell to clients with 20 to 100 employees, or for general insights into providing valuable and profitable benefits plans.